In the past bonds have been effectively used as an additional asset class to reduce the risk of holding a 100% stock portfolio. The traditional 60/40 mix of stocks and bonds has defined the moderate portfolio for years, and today target maturity mutual funds are commonly used, which will increase the bond allocation as one nears retirement to reduce the overall portfolio risk.

In the past bonds have been effectively used as an additional asset class to reduce the risk of holding a 100% stock portfolio. The traditional 60/40 mix of stocks and bonds has defined the moderate portfolio for years, and today target maturity mutual funds are commonly used, which will increase the bond allocation as one nears retirement to reduce the overall portfolio risk.

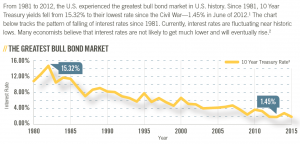

With today’s historically low interest rates, does it make sense to use bonds as an effective asset class to reduce portfolio risk? As of this writing, following the Brexit vote for the UK to leave the EU, the ten year US Treasury bond has dropped all the way to 1.37%, reaching historical lows. Eventually interest rates will rise, and when they do bonds could experience very significant losses.

Take a look at the following charts to see where interest rates have gone and the risk that has now developed in bonds. An unprecedented “bond bubble” has been created by central bank activity across the world.

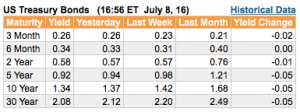

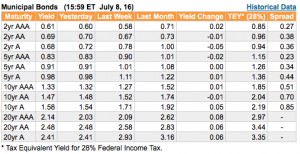

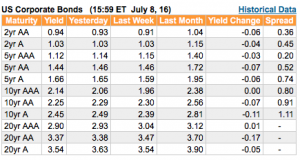

Current Bond Yields

As of this writing, let’s take a look at the yields of various bond investments available in today’s markets according to bondsonline.com

If 10 year bonds are used, which going further out in duration increases risk substantially, an investor can expect only a yield of between 1.34 to 2.45%.

Is this the right vehicle today to use to reduce risk and provide portfolio protection?

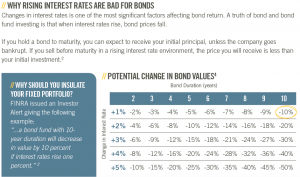

Even with this choice, as the charts above reflect, just a rise of 1% in market interest rates can cause a loss of 10% in overall value. Of course if individual bonds are used they can be held to maturity, which would return the original deposit and incur no losses. The more common bond holding that is used in today’s portfolios, are bond mutual funds which simply price the holding according to the current market value, and offer no protection to losses due to rising interest rates.

So if the goal of the use of bonds is to mitigate risk, and with rates at historical lows are they the best choice for low risk investments for investors?

Fixed and Index Annuities as an Alternative.

Safety

Both the Fixed and Index Annuity are a very safe investment that has a very low probability of loss. (See previous post on the safety of annuities.) The initial deposit and any gains that are earned, are fully protected from all types of market risk, so it is a much better option for safety than a bond portfolio. This will provide a much better buffer instead of bonds to use in a portfolio to offset the risks of owning stocks or stock mutual funds.

Both the Fixed and Index Annuity are a very safe investment that has a very low probability of loss. (See previous post on the safety of annuities.) The initial deposit and any gains that are earned, are fully protected from all types of market risk, so it is a much better option for safety than a bond portfolio. This will provide a much better buffer instead of bonds to use in a portfolio to offset the risks of owning stocks or stock mutual funds.

In fact in 2008, it was one of the only asset classes that didn’t incur losses for the investor. If we have an environment of market declines with rising interest rates, a balanced or target date portfolio, could incur much greater losses than an ivestor would have expected.

Better Returns than Bonds?

Fixed Annuity

Today one could simply use a fixed rate annuity for 5 or more years, to match or exceed the highest rate of any of the 10 year bond options, with the corporate paying 2.25%. We are seeing 5 year rates between 2.5% to 3.25% depending upon the company.

Index Annuity

If the investor would like the opportunity for higher potential returns than the Fixed Annuity, while still providing the same safety as the Fixed Annuity, one could also look at the Fixed Index Annuity. It’s very important to choose a high quality annuity that has solid crediting methods, and in doing so, based on historical rates of return, you could see returns in the 3 to 6% range. With today’s new uncapped low volatility indexes, you can design your return to be based on a variety of market sectors including bonds, stocks and commodities. (See post on low volatility indexes)

Summary

With the influence of unprecedented central bank activity that has driven interest rates to historical lows and bonds values to extreme highs, it’s time to rethink the traditional idea of using bonds to provide safety in portfolio design. If one really looks at the Fixed and Index Annuity with an open mind, you can see they provide a higher degree of safety with potentially higher guaranteed and potential returns than bonds.

Since both types of annuities are insurance products and not a security, unfortunately they are not commonly offered to clients within the brokerage and money management world, and instead are unfairly targeted as an investment to avoid. That is why it is important for all investors to take control of their portfolios and to be very objective regarding each investment opportunity. The Fixed and Index Annuity today truly is a “diamond in the rough.”